🎉 The Finance field guide is live. Learn the basics of investing, free. Read now.

Read: ≈ 4-5 min

Watch: 4 min

Quick takeaways

When you invest, more than one organisation is involved in looking after your money.

Investment platforms, asset managers, advisors, and regulators each play different roles.

Understanding the basic structure helps you know who does what and where your fees go.

What this guide covers

This guide outlines how the saving and investment industry is set up in South Africa, who the main players are, and how they interact when you open and use an investment product.

What it is

The investment industry is a network of different organisations that help you save, invest, and manage money. Each has a specific role, and together they make the system work.

In most cases, you invest through a product provider such as a platform, life company, or unit trust manager. They offer the account or product you use.

Behind the scenes, other companies manage the investments, process transactions, keep records, and hold the investments separate from the day-to-day work of the companies you interact with. Regulators set rules to protect investors and support a stable system.

You do not need every detail. You only need to know the main roles and how they connect.

Why it matters

When you understand who does what, it becomes easier to read disclosures, ask questions, and understand how products work.

You are also less likely to feel intimidated by brand names or technical language. Instead of seeing a mystery, you see a chain of responsibilities and services that you are paying for.

This awareness supports better decisions and helps you spot when something does not look or feel right.

How it works

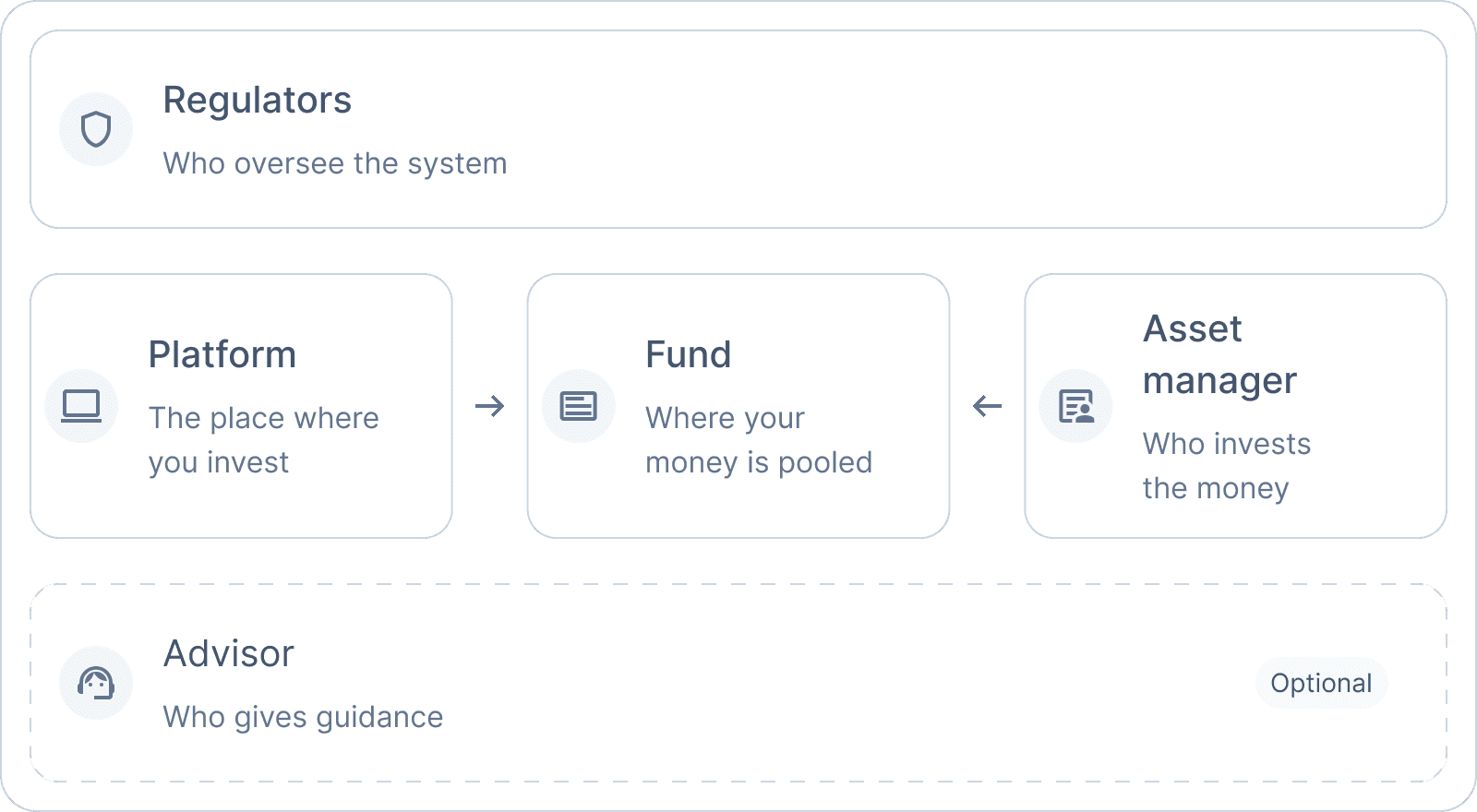

Figure 1: The industry structure

Regulators set rules for how these organisations must operate, treat clients, and disclose information. Their aim is to protect investors and support a stable financial system.

An investment platform provides a place where you can open accounts, choose products, and see your balances. It may also handle reporting, statements, and some client support.

A fund is a pool of money from many investors that is invested together. Each investor owns a share of the overall portfolio. When you invest, you choose the fund you want to be in, and the asset manager makes the day-to-day investment decisions inside it.

Asset managers are responsible for managing funds or portfolios according to set strategies. They decide what to buy and sell within the fund to meet its objectives.

Advisors, if you use one, give personal recommendations and help you choose products or strategies that fit your goals and situation. Some advisors are independent, while others are tied to particular companies.

In South Africa, different regulators oversee different parts of the system. The Financial Sector Conduct Authority (FSCA) focuses on treating customers fairly and setting conduct standards, while the South African Reserve Bank (SARB) oversees parts of the financial system that relate to money flows and stability.

Key considerations

Fees can be charged at different levels: platform, fund, and advice.

The organisation you interact with directly is not always the one managing the money.

Large, familiar brands can be reassuring, but brand alone is not a guarantee of suitability.

Some companies offer both products and advice. This can be convenient, but it may also create conflicts of interest, so it is worth asking how your advisor is paid.

Regulated companies must follow rules and provide certain disclosures, but this does not remove all risk.

Digital platforms may change how services are delivered and how fees are structured, but the core functions remain similar.

Some platforms only offer certain products or funds. If you want a wider range of choices, check the available options before opening an account.

A simple example

You may open an investment account on a platform and choose a fund managed by a separate asset manager. The platform collects your debit order, passes your money on, and shows your balance in its app or website.

The asset manager invests in shares, bonds, or other instruments inside the fund. You pay a platform fee and a fund fee. If you used an advisor to help you decide, you may also pay an advice fee.

Getting started

For each product you hold, identify the platform, the underlying manager, and any advisor involved.

Some products list both a platform and a product provider. The platform is where you interact. The product provider issues the product itself, such as a unit trust or retirement annuity.

Read the basic information documents to see who is responsible for what.

Look at the breakdown of fees and which party charges each one.

Keep a simple record so you can see your overall exposure and relationships.

When considering a new product, ask which organisations are involved and how they interact.

For most products, the Key Information Document or minimum disclosure document outlines the parties involved and their responsibilities.

Review and maintain

Check your understanding of your providers every year or when you make a change.

Companies may merge, rebrand, or update their service models over time, so it is helpful to check whether the organisations you rely on have changed.

As new digital platforms, products, or fee models appear, it helps to relate them back to the core functions you already know.

The more clearly you see the structure, the more confidently you can participate in it and the less likely you are to feel lost in the detail.

This guide is for educational purposes and is not financial advice.