🎉 The Finance field guide is live. Learn the basics of investing, free. Read now.

Read: ≈ 3–4 min

Watch: 4 min

Quick takeaways

Understanding the main types of fees and basic tax rules helps you make clearer decisions.

Small-looking percentages can add up to large amounts over many years.

Fees and taxes reduce your returns, which slows down compounding.

What this guide covers

This guide explains how fees and taxes affect your investment outcomes over time, outlines the main types of costs you may see, and offers simple ways to pay attention to them without getting overwhelmed.

What it is

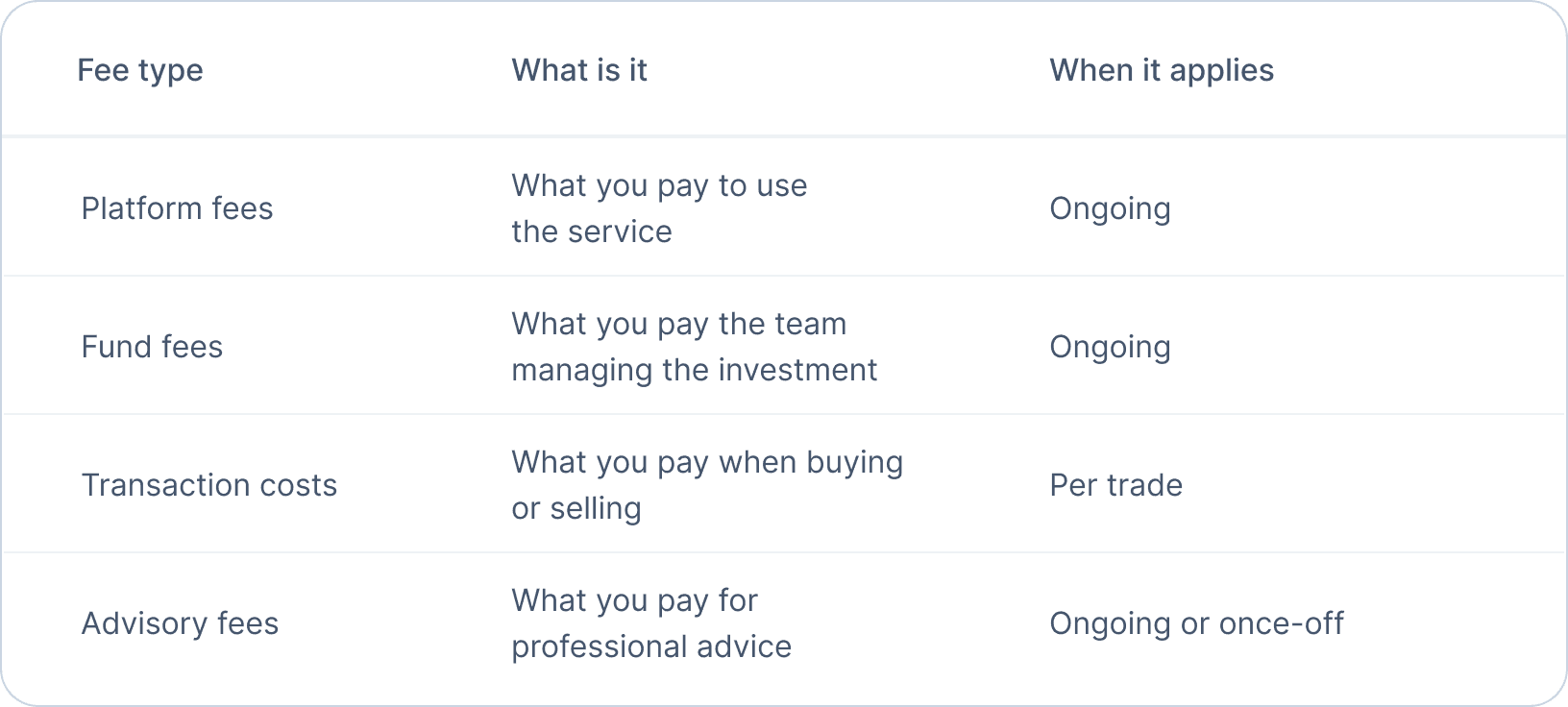

When you invest, you may pay different types of fees. These can include platform fees, fund fees, transaction costs, or advisory fees.

Each fee is a cost that comes out of your investment.

Figure 1: Types of investment fees

Some products offer tax benefits, such as tax-free savings accounts, while others may be taxable.

Taxes are amounts you may need to pay on certain types of investment income or gains, depending on the product and the rules that apply. This may include tax on interest, dividends, or capital gains.

You do not need to memorise every detail, but you do need to understand that these costs reduce what you keep.

Why it matters

Over one year, a one percent difference in fees may seem small. Over twenty or thirty years, it can add up to a significant difference in what you end up with.

Fees and taxes reduce your net return. This means less money stays invested to benefit from compounding. Two people who invest the same amount for the same time in similar markets can end up with very different outcomes if one pays higher ongoing costs.

Paying attention to fees and using tax-efficient products where appropriate is one of the few parts of investing that you can control.

How it works

Fees are usually charged as a percentage of the amount you have invested, a flat amount, or a mix of both. Some are taken monthly or annually, others apply when you trade or switch investments. Ongoing fees are often taken automatically from your balance.

Taxes depend on the type of income or gain and on the rules that apply to your situation. Some products are designed to shelter you from certain taxes up to set limits, while others are fully taxable.

You will often see total cost figures expressed as an annual percentage. The higher this percentage, the more of your return you give up each year.

Key considerations

Look at the total cost, not just one fee in isolation.

Be wary of products that are hard to understand or that hide costs in complex structures.

A lower fee is not always better if it comes with poor service or an unsuitable product, but unjustified high costs are a red flag.

Tax-free or tax-efficient products can be powerful tools when used correctly and within the rules.

Written disclosures and statements are important sources of information. Take time to read them.

Review your fees and taxes regularly.

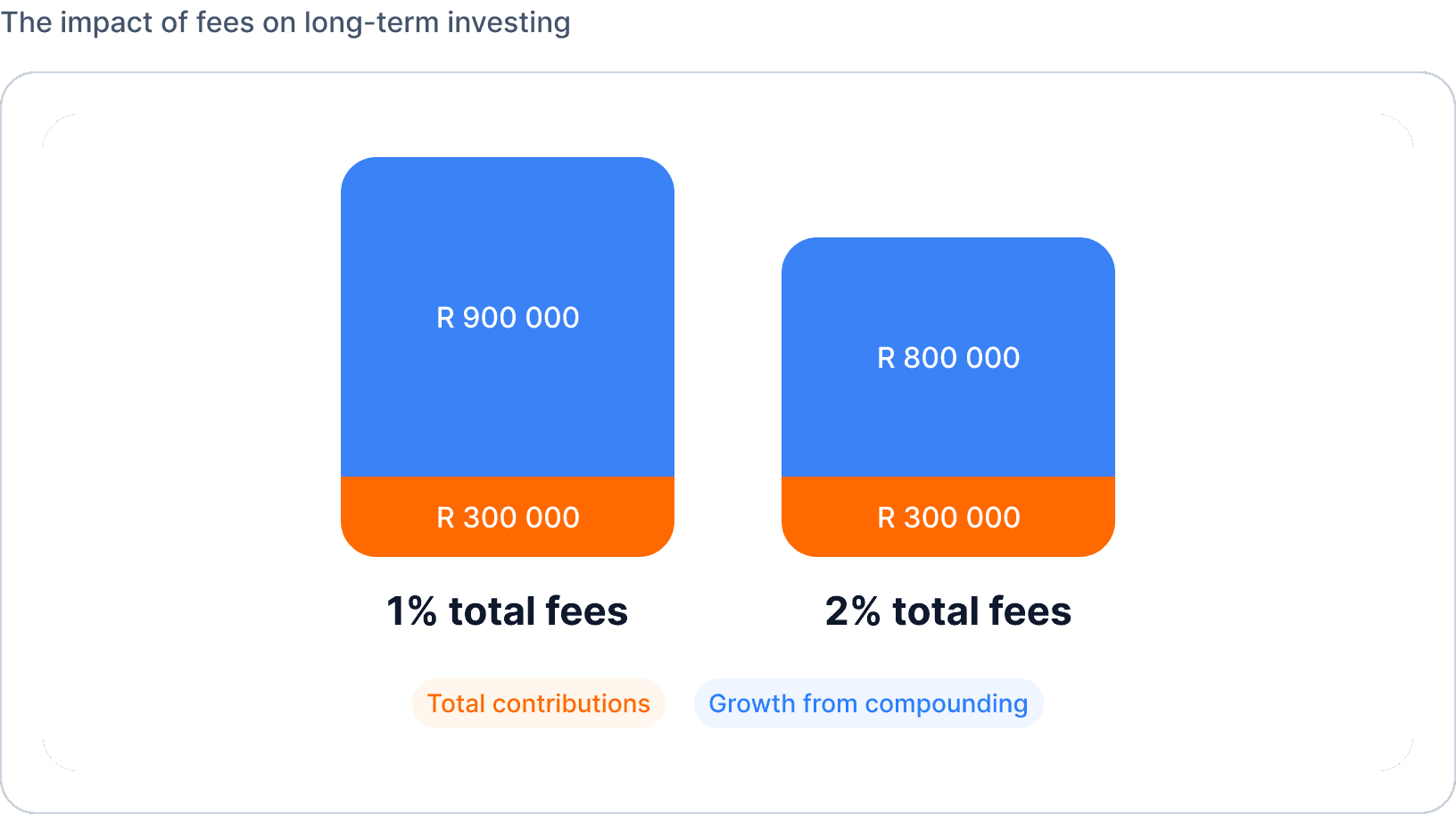

A simple example

Imagine two people each invest R1 000 per month for 25 years. They earn the same gross return, but one pays one percent per year in total fees and the other pays two percent.

Both contribute R300 000 over the period. The person paying higher fees ends up with a noticeably lower final amount because more of the growth has been taken as costs each year and less money compounds.

The difference comes entirely from the higher ongoing costs.

Figure 2: The impact of fees on long-term investing

Getting started

Make a list of your existing savings and investments.

Look for information on the total fees for each product. Some fees may sit in different parts of a statement, so check more than one place.

Note which products have tax benefits and what limits apply.

Ask direct questions when you are unsure what you are paying for.

Before opening a new product, compare its costs and tax treatment to what you already have.

Review and maintain

Review fees and tax implications at least once a year or when you make a major change. Costs that seemed acceptable at first may not stay competitive over time.

You may not be able to avoid all fees or all taxes, but you can avoid unnecessary or excessive ones. Over the long term, keeping more of your return working for you can make a meaningful difference.

This guide is for educational purposes and is not financial advice.