🎉 The Finance field guide is live. Learn the basics of investing, free. Read now.

Read: ≈ 4-5 min

Watch: 3 min 45

Quick takeaways

Investing success depends heavily on your habits and decisions, not only on when you enter or exit the market.

Trying to time markets perfectly is extremely difficult, even for professionals.

Simple behaviours, such as staying invested, contributing regularly, and avoiding panic decisions, can support better outcomes over time.

What this guide covers

This guide explains why your behaviour plays a larger role than market timing in your long-term results, and outlines practical habits that make it easier to stick with your plan.

What it is

Behaviour in this context refers to how you act and react around your money. It includes how often you check balances, how you respond to news, and whether you follow or ignore your own plan.

Market timing is the attempt to predict when markets will rise or fall, and to move money in and out at just the right moments.

Research and experience show that behaviour is easier to influence and usually more reliable to focus on than trying to predict short-term market moves.

Diversification helps share risk, but your behaviour determines whether you stay invested long enough to benefit from it. Even a well-diversified portfolio can deliver weaker results if you move in and out at the wrong moments.

Why it matters

The biggest risk for most beginners is not choosing the wrong investment, but reacting to normal market changes in ways that harm long-term growth.

Large market moves and news headlines can trigger strong emotions. Fear may push you to sell during a downturn. Excitement may tempt you to chase whatever has recently done well.

These reactions can lead to buying high and selling low, which works against long-term growth. Missing just a few strong recovery days after a downturn can have a big impact on long-term returns.

These powerful “rebound” days often happen early in a recovery, usually when confidence is still low. If you sold during a downturn and only reinvest after markets feel safer, you are likely to miss them. A single missed rebound does not seem serious, but missing several can add up over decades.

On the other hand, simple, steady actions such as contributing regularly, staying invested, and avoiding unnecessary changes can help you benefit from long-term trends without needing perfect timing.

How it works

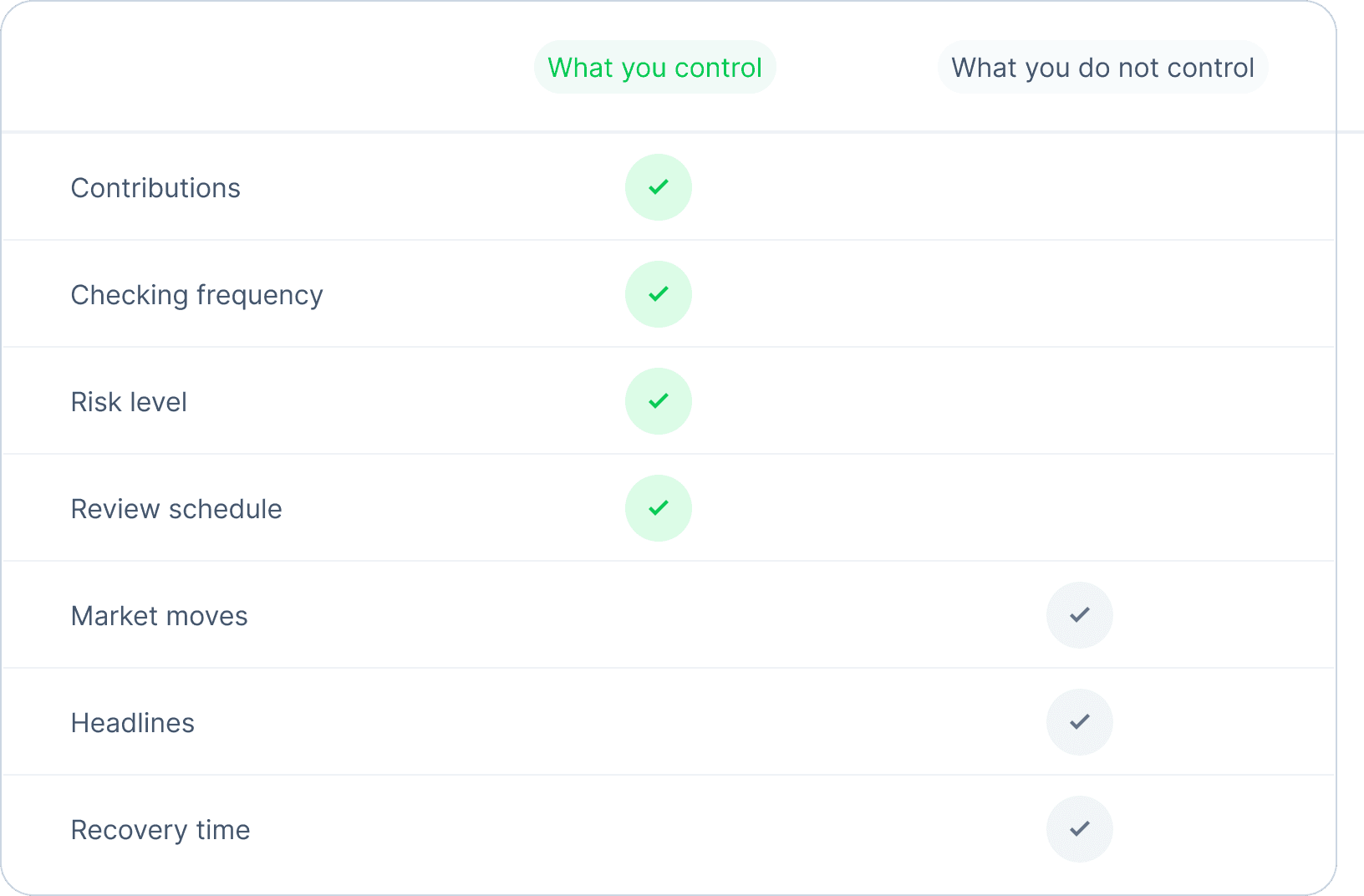

You cannot control the market, but you can control your plan and your responses. This includes deciding in advance how much risk you are comfortable with, how long you plan to invest, and how you will respond when markets fall.

A quick comparison helps show where to focus your attention.

Figure 1: A comparison of factors investors can control versus those they cannot control

Putting systems in place helps. Examples include automatic contributions, scheduled check-ins rather than constant monitoring, and clear rules for when you will make changes.

By shaping your environment and habits, you reduce the chances that momentary emotion will drive major decisions. Many beginners find that checking their balance too often makes normal ups and downs feel larger than they are, which increases the temptation to act quickly rather than follow their plan.

It is normal to feel uneasy during market swings, which is why setting simple rules ahead of time can make difficult moments easier to navigate.

Key considerations

Markets will move up and down. Volatility is part of investing, not a sign that something is broken.

Trying to move in and out based on short-term predictions is very hard to do well and consistently.

Downturns are normal and expected. A well-built plan assumes they will happen, so short-term drops do not mean the plan is failing.

Your risk level should be set so that you can sleep at night, even during downturns.

A written plan makes it easier to stay calm when conditions change.

Talking to a trusted person can help you pause before making large, emotional decisions.

A simple example

Two investors each commit to investing R1 000 per month for 25 years. One sticks to the plan, investing the same amount each month regardless of headlines. The other stops contributions and sells during every downturn, then returns only after markets have already recovered.

They put in the same total amount, but the investor who stayed the course is likely to end up with a higher value, because more money stayed invested during recovery periods.

The reason is simple: more of their money stayed invested during the periods when markets recovered the most. Even small gaps in time out of the market can reduce the long-term total.

Getting started

Write down your main financial goals and approximate time frames.

Choose a level of risk you feel you can live with through ups and downs.

Set up automatic contributions where possible.

Decide how often you will review your investments, for example once or twice a year.

When you feel a strong urge to act based on news or fear, wait a set period before making any major move.

Decide ahead of time how you will respond if markets fall sharply. Having this written down makes it easier to stay calm and follow your plan.

Review and maintain

Review your plan and behaviours once a year. Notice which habits support your goals and which make you anxious or lead to frequent changes.

With a clear plan, a diversified portfolio, and calm, consistent habits, you give yourself the best chance of benefiting from long-term growth without needing to predict what markets will do next.

Over time, these simple actions put you in control of what matters most.

This guide is for educational purposes and is not financial advice.