🥳 Good news! Under 30s now pay R50/month for a Protea subscription. See pricing page.

Read: ≈ 4 min

Watch: 4 min

Quick takeaways

An emergency fund is money set aside for unexpected costs so that you do not need to borrow or sell investments at a bad time.

A common starting point is to aim for three to six months of essential expenses, but any amount is better than none.

Keeping emergency money separate from day-to-day spending helps you avoid dipping into it for non-urgent things.

What this guide covers

This guide explains what an emergency fund is, why it should come before investing, how much to aim for, and simple steps to get started, even if money feels tight.

What it is

An emergency fund is a separate pool of money that you keep for real emergencies. These are unplanned events that affect your health, your job, your home, or your ability to earn an income.

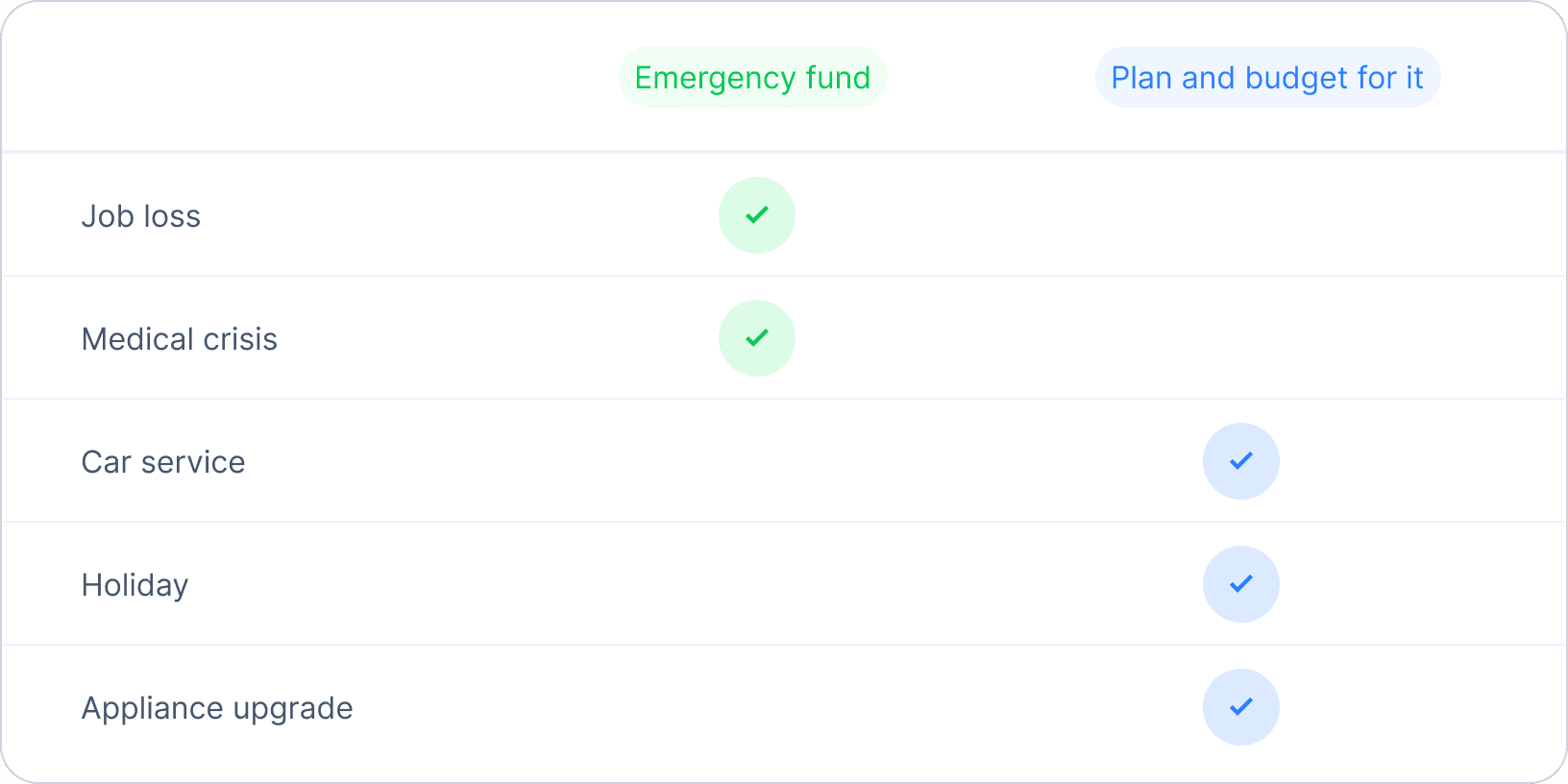

Examples include losing your job, an unexpected medical bill, emergency travel, or a major car repair. It is not there for planned expenses like holidays, birthdays, or routine car services.

The goal is simple. When life happens, you have cash available so that you do not need to swipe a credit card, take out a loan, or cash out long-term investments at a bad time.

Figure 1. Example of what to use your emergency savings for

Why it matters

Without an emergency fund, surprise expenses tend to turn into debt. High-interest debt can grow quickly and make it harder to move forward with any financial goal.

An emergency fund gives you breathing room. It buys time to make thoughtful decisions instead of rushed ones. It also makes it easier to keep long-term investments in place during market ups and downs, because you are not forced to sell when you need cash.

Even a small buffer can make a big difference. The habit of setting money aside for emergencies builds confidence and reduces stress.

How it works

You decide on a realistic target, for example one month of essential expenses, and save towards it consistently. Essential expenses are the things you must pay to keep your life running, such as rent, food, transport, and basic bills.

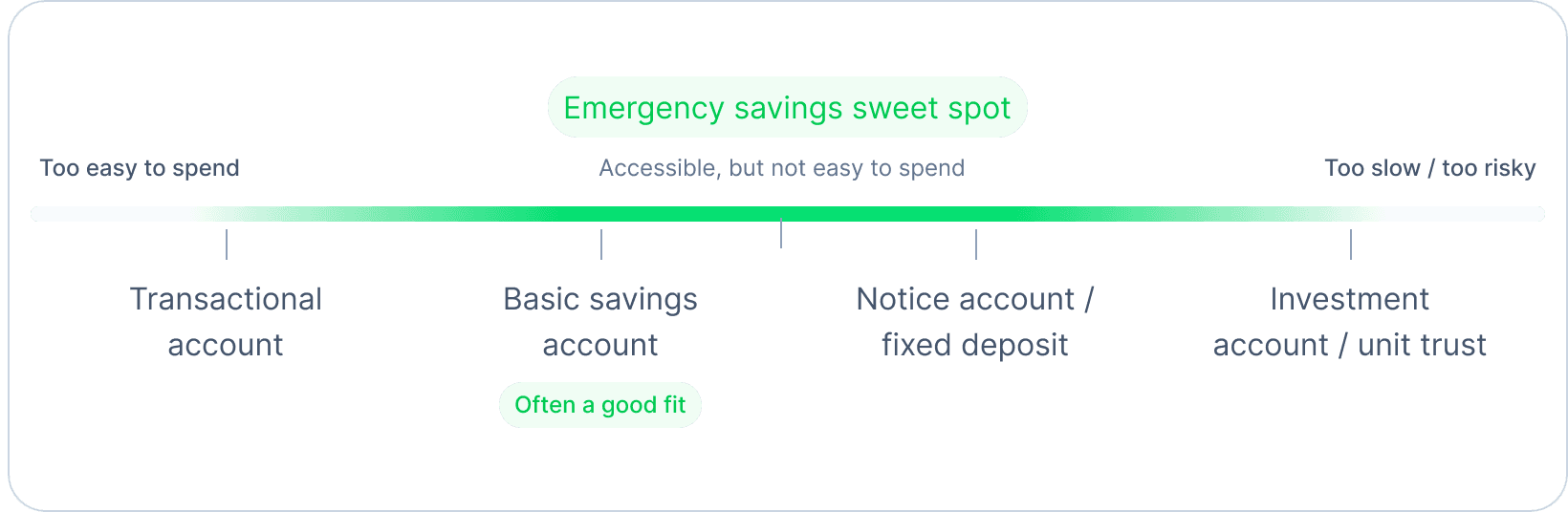

The money should be easy to access, but not so easy that you spend it without thinking. Many people use a separate savings account or savings pot to keep this money apart from daily spending.

An emergency fund is not meant to grow fast. Safety and access are more important than return. Once you have built a solid base, you can focus on longer-term investments that aim for growth.

Figure 2. Emergency savings sweet spot

Key tips

Start with a small, achievable goal if three to six months feels impossible.

Keep the money in a low-risk place where you can access it within a few days.

Automate a monthly transfer into your emergency savings if possible.

Only use the fund for genuine emergencies, not for wants or planned expenses.

If you use it, make a plan to rebuild it once the crisis has passed.

A simple example

Imagine your essential monthly expenses are R8 000. A three-month emergency fund would be R24 000. That amount may feel out of reach at first.

If you start by saving R500 per month, you will have R6 000 after one year. It is not the full target, but it already gives you more security than having nothing set aside.

Getting started

List your essential monthly expenses to understand how much you will need per month.

Choose a first target such as half a month or one month of expenses.

Open or set up a separate place for emergency savings.

Decide on an amount you can save regularly, even if it is small.

Review your progress every few months and adjust your target over time.

Review and maintain

Check your emergency fund at least once a year or when your life changes. If your costs increase, you may need a larger buffer. If you have had to use the fund, rebuild it before increasing long-term investments.

The goal is not perfection. The goal is to have something in place so that the next surprise is less likely to push you into expensive debt.

This guide is for educational purposes and is not financial advice.